Adaptive VWAP Volume Weighted Average Price Institutional MT5 Indicator | Free Download

$0.00

Adaptive VWAP Institutional MT5 Indicator is a precision engineered, institutional grade Volume Weighted Average Price (VWAP) tool for MetaTrader 5. Designed for high-frequency trading (HFT), professional asset managers, and serious intraday traders, it delivers DST aware session calculations, asset class autodetection, volatility filtering, and zero-latency persistence bringing institutional data standards directly to your MT5 platform.

Description

What makes the Adaptive VWAP Institutional MT5 Indicator different from a regular VWAP indicator?

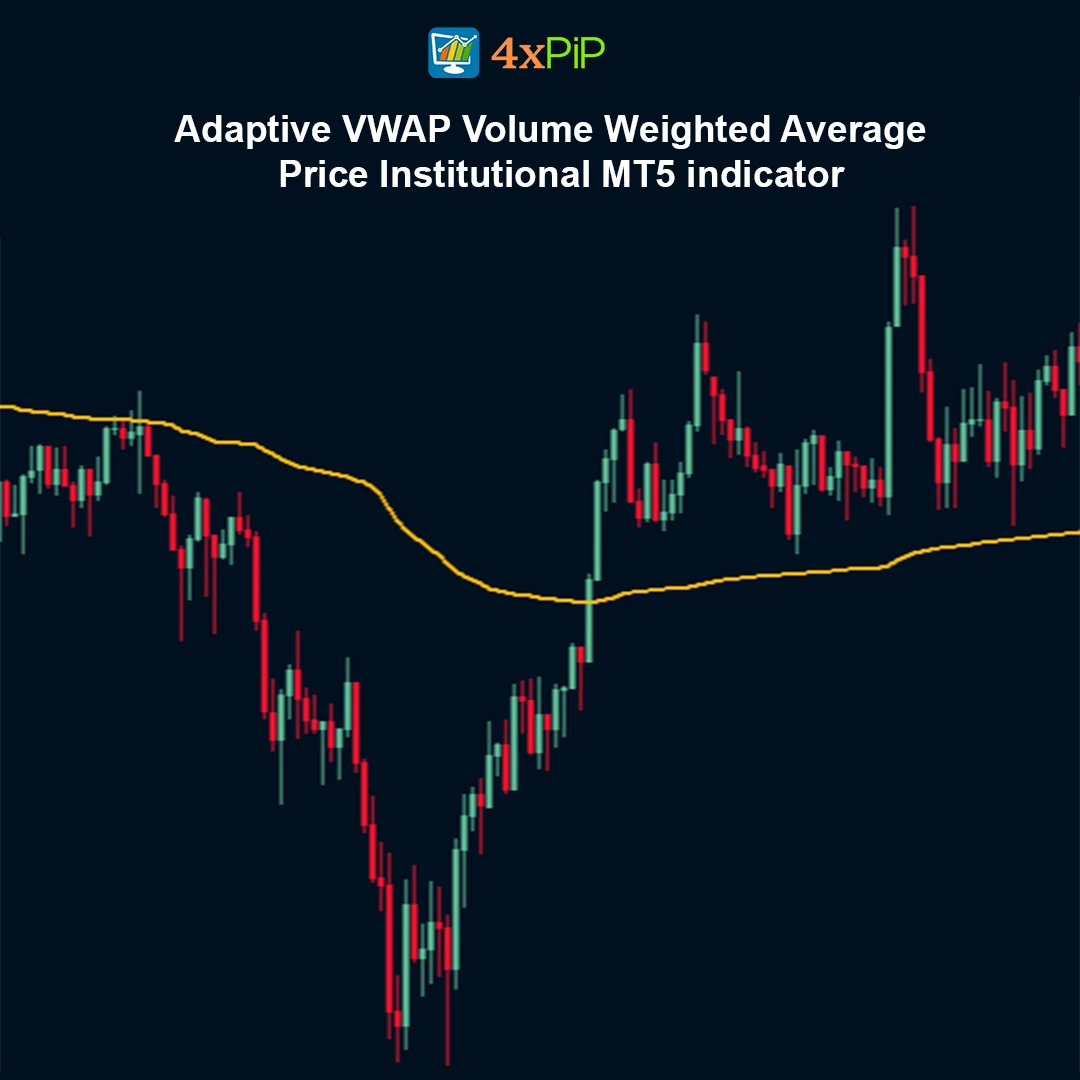

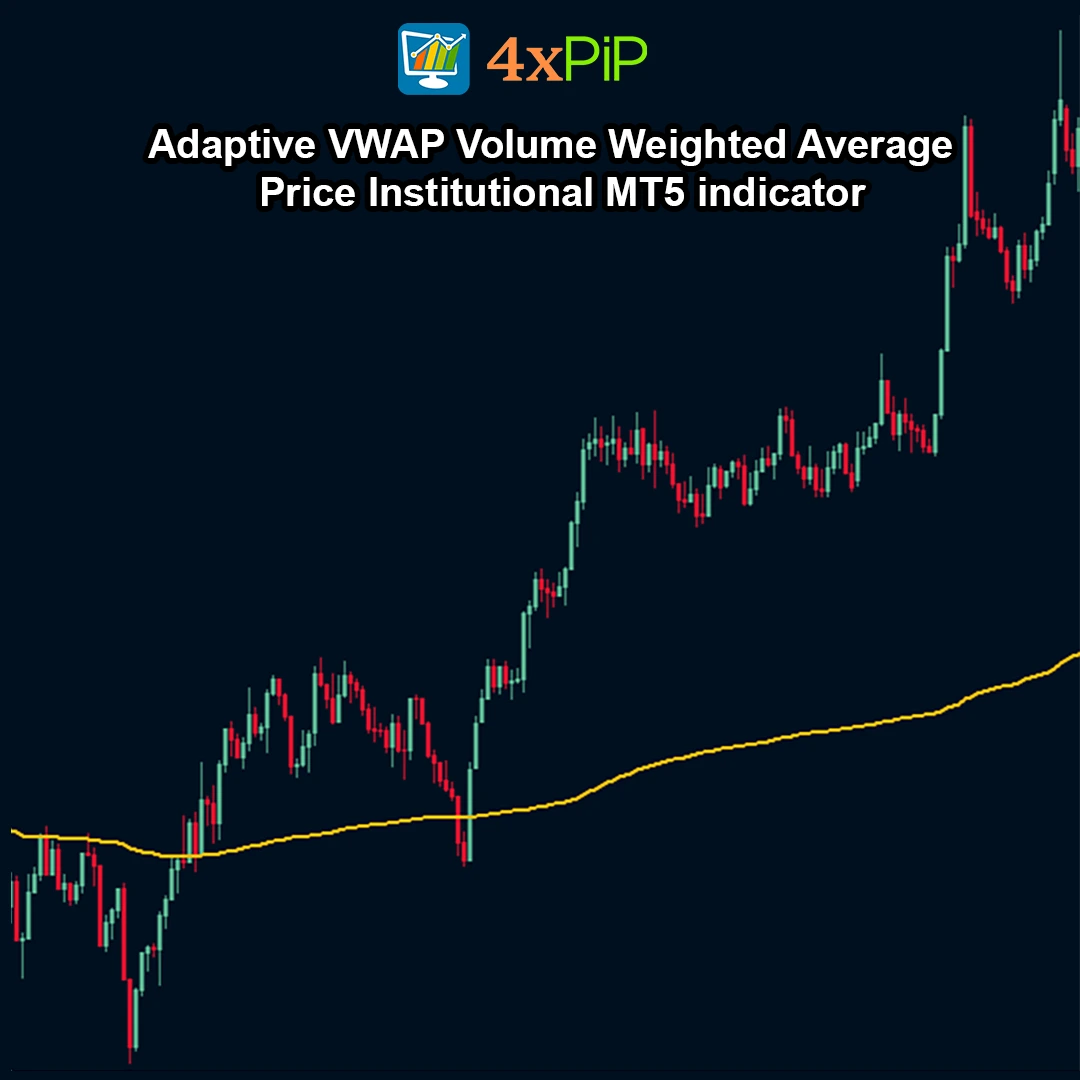

The Adaptive VWAP Institutional MT5 Indicator is designed to operate at an institutional level rather than functioning as a simple retail VWAP tool. Traditional VWAP indicators only calculate the average price based on volume for a given session, while this indicator includes advanced analytical systems that improve accuracy and reliability. It automatically adapts to different market structures, filters abnormal volume activity, and ensures precise session calculations. These capabilities make it more suitable for professional traders who require stable and precise market analytics. As a result, traders receive a much clearer view of price positioning relative to institutional trading activity.

How does the indicator automatically detect different asset classes?

One of the most powerful components of this indicator is its multi-stage asset intelligence system. This system automatically recognizes the type of asset being traded, whether it is Forex, cryptocurrency, metals, stocks, or indices. After identifying the asset class, the indicator applies the appropriate reset policy and trading session structure for that market. This eliminates the need for traders to manually adjust settings when switching between different instruments. By automating this process, the indicator reduces configuration errors and ensures that VWAP calculations remain accurate across all supported markets.

How does the Institutional Timezone Engine improve session accuracy?

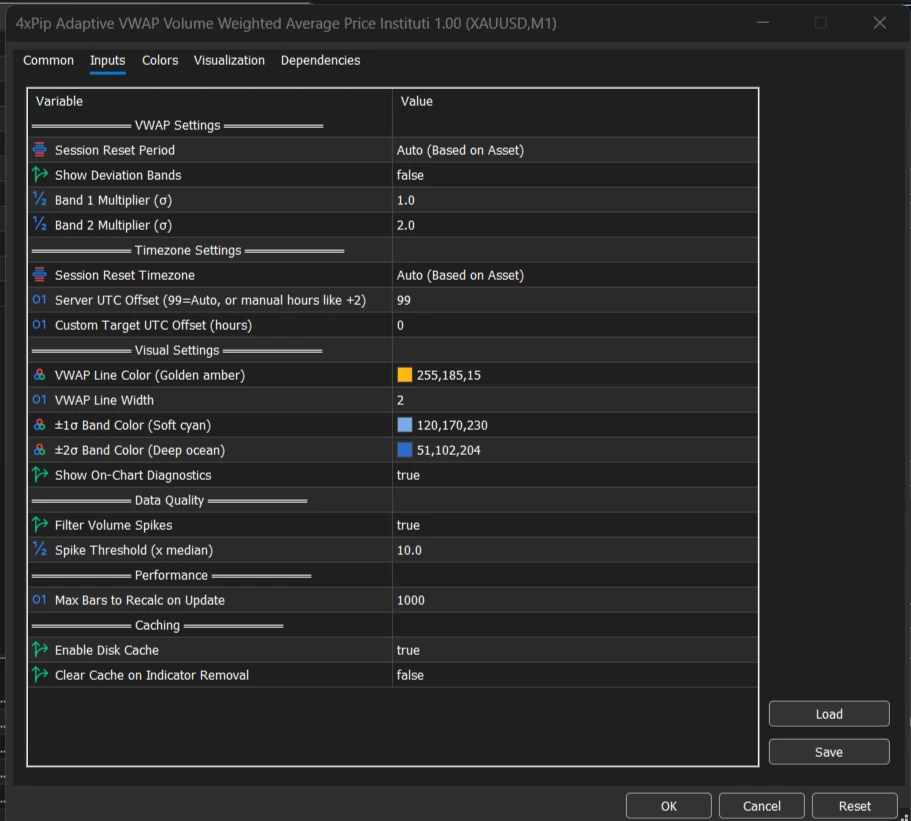

The indicator features an advanced Institutional Timezone Engine designed to ensure accurate market session calculations. It is fully aware of Daylight Saving Time (DST) adjustments and uses the mathematical Zeller’s Congruence algorithm to determine correct trading sessions. This allows the indicator to calculate session boundaries for major financial hubs such as New York, London, Tokyo, and Sydney with high precision. Accurate session timing is crucial because VWAP resets and calculations depend heavily on the correct market opening and closing periods. By automating this process, the indicator ensures consistency regardless of broker server time or seasonal time changes.

Why is the 17:00 New York rollover important for Forex and commodities?

The 17:00 (5 PM) New York rollover is considered the industry standard reset time for many Forex and commodity markets. Institutional traders typically use this time to mark the end of a trading day and begin a new session. The Adaptive VWAP Institutional MT5 Indicator supports this rollover automatically, ensuring that VWAP calculations align with professional trading practices. This is particularly important for markets such as Gold, oil, and currency pairs where session boundaries significantly impact volume distribution. By following this industry-standard timing, the indicator provides data that is consistent with institutional trading analysis.

How does the volatility-adaptive median volume filter improve accuracy?

Financial markets often experience irregular price movements caused by bad ticks, data spikes, or sudden institutional order bursts. These anomalies can distort the VWAP calculation and create misleading signals for traders. To solve this problem, the indicator includes a volatility-adaptive median volume filter that analyzes incoming volume data and filters abnormal values. By neutralizing these irregular spikes, the VWAP line remains smoother and more reliable during volatile market conditions. This results in more accurate price positioning relative to the true market average and helps traders avoid false signals caused by data irregularities.

Advantages

- Institutional grade calculation precision

- Automatic asset class detection and reset logic

- DST aware global session accuracy

- Forex-standard 17:00 New York rollover support

- Median volume filtering to remove bad ticks

- High-speed disk caching for session persistence

- Low-latency optimized execution loop

- Professional real time diagnostic panel

- Customizable deviation bands (±σ)

- Fully adaptable for intraday and multi-session trading

Features

- Multi Stage Asset Intelligence (Crypto, Forex, Metals, Stocks, Indices detection)

- Institutional Timezone Engine using Zeller’s Congruence

- 17:00 New York session reset for Forex & commodities

- Volatility adaptive median volume sampling

- Zero-latency disk caching persistence

- Modular high-performance O(n) architecture

- Real-time VWAP distance percentage display

- Session accumulated volume tracking

- Adjustable spike threshold for noise filtering

- Configurable historical depth (Max Recalc Bars)

How to Trade

The Adaptive VWAP indicator can be used in multiple trading approaches depending on market conditions. Traders commonly begin by using VWAP for trend confirmation: when the price trades above the VWAP line it generally signals a bullish bias, while price below VWAP suggests a bearish bias. In trending markets, VWAP often works as dynamic support in uptrends and dynamic resistance in downtrends, helping traders identify potential pullback entry points.Another popular method is the mean reversion strategy, where price moving far away from VWAP especially beyond the ±1 or ±2 standard deviation bands indicates that the market may be overextended and likely to return toward the VWAP level; traders typically wait for reversal signals before entering counter trend trades.

The indicator is also useful for momentum breakout trading, as a strong move through the VWAP line accompanied by increasing volume can signal institutional participation and the continuation of a trend. Additionally, VWAP works well in session-based trading, where intraday traders often use daily VWAP resets while swing traders may anchor VWAP to weekly or monthly sessions to identify broader institutional price levels. Overall, VWAP also highlights institutional liquidity zones, since repeated price reactions around the VWAP line often indicate areas where large market participants are accumulating or distributing positions, helping traders refine their trade entries and confirmations.

Formula

VWAP Calculation Methodology

The indicator is based on the standard Volume Weighted Average Price (VWAP) formula:

VWAP = Σ (Price × Volume) / Σ Volume

Where:

- Price = Typical Price = (High + Low + Close) / 3

- Volume = Tick volume or real volume (depending on your broker feed)

Deviation Bands:

Upper Band = VWAP + (σ × Standard Deviation)

Lower Band = VWAP – (σ × Standard Deviation)

The Adaptive VWAP enhances this calculation by:Applying session based reset logic.Filtering abnormal volume spikes via median sampling.Maintaining session persistence through disk caching

Conclusion

The Adaptive VWAP Institutional MT5 Indicator bridges the gap between retail charting tools and institutional grade analytics. With automated asset detection, DST aware session handling, advanced filtering, and high-performance execution, it provides a professional framework for trend confirmation, liquidity mapping, and mean reversion trading.

Engineered for precision, optimized for performance, and built for traders who demand institutional accuracy ,this is more than a VWAP. It is a complete session-based analytical engine.

DOWNLOAD NOW Reach Us on WhatsApp

Reach Us on WhatsApp Fly Over to Telegram

Fly Over to Telegram Drop Us an Email

Drop Us an EmailFAQ's

Q & A

Related products

-

Premium

PremiumForex Scanner: Dashboard Scanner for MT5 | Market Scanner

Original price was: $299.00.$199.00Current price is: $199.00. Select options -

Free

FreeMT5 EA Drawdown Limiter

Original price was: $100.00.$10.00Current price is: $10.00. Select options -

Free

FreeAuto Risk-Based Lot for MT5 EA

$30.00 Select options -

Free

FreeMT5 MACD Explained Indicator

$0.00 Select options

Reviews

There are no reviews yet